Banking Industry in today's Economy

New realities of Banking industry in India

Shuchi.P.Nahar

India’s banking sector is a study in contrasts: it supports the world’s fastest-growing large economy but is grappling with challenges that test its strength and resilience. Primary among them is the burden of distressed loans. According to Reserve Bank of India (RBI) data, the value of banks’ gross nonperforming assets (GNPA) and restructured assets reached $250 billion in April 2019 and has been growing by almost 25 percent year on year since 2013.

India’s banking sector is a study in contrasts: it supports the world’s fastest-growing large economy but is grappling with challenges that test its strength and resilience. Primary among them is the burden of distressed loans. According to Reserve Bank of India (RBI) data, the value of banks’ gross nonperforming assets (GNPA) and restructured assets reached $250 billion in April 2019 and has been growing by almost 25 percent year on year since 2013.

State-owned banks account for more than three-fourths of the stressed-asset load, which is now far higher than their net worth. Provision levels are inadequate because these banks hold only 28 percent of GNPAs and restructured assets as provisions. There is a gap of close to $110 billion between the system’s stressed assets and the provisions made. These problems are considerably less severe for private banks.

Banking industry are very crucial to the economy that half of the industry is backed by federal insurance and have generic financial product.

There is no particular formula to know why one

bank is better than others but they have their own traits .

It's all about the risk they take , the banks accept three types of risk:

a. Credit

b. Interest rate

c. liquidity

The people hand over the money to bank so that they can manage the risk even more cheaply,

this is what bank exactly earn- managing the risk.

Credit Risk:

Everything we learn about the bank such as balance sheets , loan categories , trends in NPA

gives us an idea about what the bank was today and not what it could be in the future.

Banks have three unique ways to shield from risk unlike others

a.portfolio diversity

b.conservative underwriting and account management

c. aggressive collection procedures

The best way is to diversify loan(companies, industries,geographies) ‘when you own bank 100$

its your problem but when you owe them 100 mn$ it is the bank’s’ problem.

To manage this risk it can borrow on large varieties of loan or buy and sell loan portfolios.

Solid underwriting and collection procedures

In a bank its important to spot credit quality problems there should be focus on charge off rates

and delinquency rates to know future charge offs .

A delinquency rate is the percentage of

loans within a loan portfolio that have delinquent payments. A delinquency rate can be further broken down by categories. It is common for lenders to provide delinquency levels by both length of delinquency and delinquency by credit quality category.)

(The charge off rate is the amount of charge offs divided by the average outstanding

credit card balances owed to the issuer. Charge off is actually an accounting term that

means a company has decided it has no chance to collect a debt and charges it off its books)

The best regional banks saw their charge off rise easily in latest economic downturn ,

there are many cases like this , thus look for them in SEC reports and pay heed to what the management has to say, a good team will outline the trend properly.

Look out for extreme fast growth , not all growth is bad but if it exceeds abnormally then

the competitor , its bad. In Financial industry abnormal growth has always lended up in big

trouble.

Check the credit culture is sound or not, for example looking at charge off and delinquency ratio , reading annual reports, what kind of economic environment does the bank operate in.

Liquidity:

It's the second biggest risk bank would face , the bank can get an edge if its prepared of immediate liquidation of loan provision , for eg: many businesses pay standing fee in order to maintain a back up line for credit , bank sells nothing but a promise.

Check to see if deposits are increasing or decreasing, mainly savings and current.

(categories)

Also check out banks that provide loans to multiple sectors and how have they changed overtime.

Diversification in risky auto loans when they had been mortgage lending banks make

investors wonder that the company has multiple experience or understanding towards

giving that type of loans.

Interest Rate Risk:

It is not in control of the bank ,the bank rate is often simplified to ‘ higher rates, good. Lower rates ,bad.’

The bank can be either asset sensitive or liability sensitive , but in recent times bank tries to ensure equal rates of both , we cannot always consider the bank this helpless.

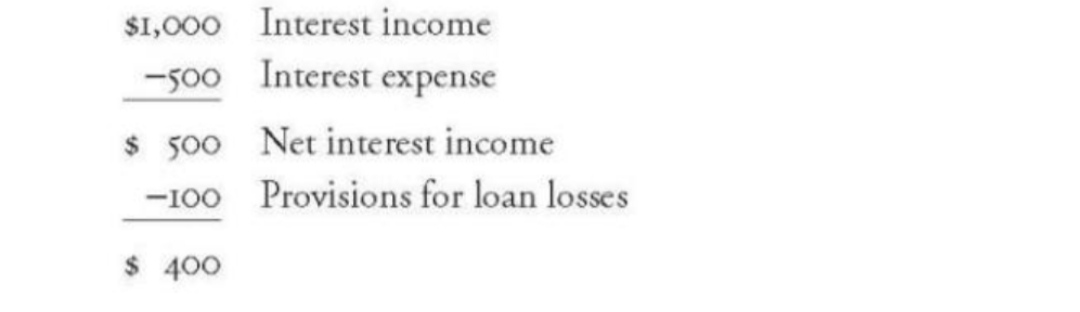

In the books of accounts we have,

Now let's assume that non interest income is comparatively stable and is kept constant

Now let's assume that non interest income is comparatively stable and is kept constant

In the books of accounts we have,

The ideal calculations are as follows

The fed has cut rates, there are some clues passed on to the bank so if they are not liability sensitive, they can reposition themselves and widen NII.

The fed has cut rates, there are some clues passed on to the bank so if they are not liability sensitive, they can reposition themselves and widen NII.

Now incase of weak economy like lower employment rate, the provisions increase . this type of scenario is common but the big banks have an edge to concentrate on one sector then other , due to widespread reach and have the ability to access the capital markets (bond), and by doing so, they can focus on their main credit and liquidity management.

The economic moats in bank

a. Huge balance sheet requirements

b. Large economies of scale

c. A regional oligopoly type structure

d. Customer switching cost

Economies of scale :

Banking offers huge economies of scale , the revenue per employee has increased dramatically

proving employee compared to old times have increased their productivity despite 44% of banks

closing in US.

Market oligopolies :

The industry has become concentrated on the regional level eg: bank of america or the credit

card industry that leaves rest of the player very helpless on commanding.

Customer switching:

Bank has very loyal customers, partly due to branding or inertia Look out for strong capital base, its basic to look at equity to asset ratio , its difficult to give rule of thumb, because it depends on riskiness of its loan but most of the banks have 8-9% capital ratios in

range ,also look for loan loss to NPA.

Return on equity and assets :

They should generate mid to high teen numbers

Operating cost as a percentage of net revenue , many have it under 55%, the lower the better.

NIM: Net Interest Margin

NIM% of average assets , most of them fall in 3-4% range , try to check a trends , also

NIM% of average assets , most of them fall in 3-4% range , try to check a trends , also

compare it with interest rates ( less interest rate, higher the margin)

Keep eye on three major metrics:

A.NIM

B.Fee income growth

C. Fee income as % of revenue

Compare with similar institution and make sure to look over the trend.

Price to book value :

Assuming that their assets and liabilities is close to approx value in the balance sheet, p/b is a

good ratio to value the banks , anything above that, the bank is paying

Seldom do banks trade at less than book value, if they do, they have their assets distressed.

Any bank trading, less than 2 times of book value is worth having a closer look at

All this could have been the starting point but you need healthy sense of skepticism.

Conclusion:

India’s banking sector is at a crossroads. Traditional players face huge disruptions, while digital growth is propelling changes in technology and customer mind-sets. This period of disruption presents tremendous growth opportunities. Old banks will need to make bold moves and initiate major transformations to take advantage of them. The path for new players, which are not saddled with the problems of the past, and for existing but relatively unconstrained banks is considerably easier. Those that master these new realities could build truly world-class banking businesses at scale.

Conclusion:

India’s banking sector is at a crossroads. Traditional players face huge disruptions, while digital growth is propelling changes in technology and customer mind-sets. This period of disruption presents tremendous growth opportunities. Old banks will need to make bold moves and initiate major transformations to take advantage of them. The path for new players, which are not saddled with the problems of the past, and for existing but relatively unconstrained banks is considerably easier. Those that master these new realities could build truly world-class banking businesses at scale.

Source : Mc kinsey reports

Banking Metrics

Banking Metrics

Shuchi.P.Nahar

Comments

Post a Comment