Art of Investing by - Sajal Kapoor

Art of investing by - Sajal Kapoor

Background

Sajal Kapoor is into the operational risk and regulatory compliance industry and within that industry, he has been working across domains from banking to healthcare to investment forms.

Over the last 20- 25 years and that has been highly rewarding and productive because,

That gave him the opportunity to look at the world from a risk and compliance point of view.

Experience that he got from the industry, experience working through banks and healthcare firms, consultancies, and investment firms gave him a sort of a different perspective, and somewhere in the background starting around the mid-90s this hunger and drive to know more about this animal called Mr. market and that started emerging.

It has been a very long and rewarding journey it has had its own sort of ups and downs like any investor goes through and but those ups and downs are like the tuition fee that you pay and you get to get yourself up and running and so after some initial hiccups and there was an IPO boom going on in mid-nineties some money was lost of experience and he is always hunting for that unknown, unseen undiscovered and potentially undervalued business somewhere and that's being his journey.

Sajal Kapoor has also tried and restricted himself to the pockets where he has got some sort of inherent advantage. So he restricts himself to 3-4 sectors only and that kills the 80% of the universe. He will not even consider looking at that and by so its his professional and investing passion combined together that gave him a lot of unseen perspectives.

Investing Framework- Seven Core Pillars

All seven pillars are important. Emphasizing one over the other will not justify the essence of the investing framework.

One important lesson for all we need is to keep learning, keep evolving and this is not done instantly, any imagination or sort of a rigid framework will keep evolving and as you go along.

Investing as we know is all about continuous learning so the moment you stop learning you'll start crashing.

Circle of Competence

Management

Industry structure

Business economics

Psychology

Narrative and Numbers

Cycle and valuations

- Circle of Competence

Over a period of time after losing money in certain sectors and gaining disproportionately and some of the other sectors coupled with his sort of professional career and background he understood that it's very important to stick to your circle of competence.

As Warren Buffet says it doesn't matter how big your circle of competence is as long as you know the boundaries and that's fine and the whole benefit of staying inside the circle of competence is that you don't have to be better than and everyone everywhere right and so you just aim to win in the league in which you play.

And the league in which Sajal Kapoor plays is all about sustainable long-term compounding businesses the pharmaceuticals be chemicals he has played some autos as well these are the four key pockets.

He has played over the years and as I call them that circle of components is tend amount

to circle of luck so the more you shrink your circle and the greater your luck quotient goes up the other thing is that it's easy to learn from your mistakes.

So if you are playing within a restricted sort of COC and mistakes will tend to happen mistakes as Sajal Kapoor says he has made mistakes in pharmaceuticals, made mistakes in FMCG and he has made mistakes even in my very small tiny circle.

But you will find it easier to learn from those mistakes because you know the boundaries of yours and of your circle of competence and there was a tweet that he did last year from Joel and that said that “choosing individual stocks without any idea of what you are looking for is like running through a dynamite factory with a burning match. you may live but you are still an idiot” because you don't know what you don't know and that's the reason and defining a circle of competence is important.

Basic General guidance to new entrants

Quest: If someone wants to invest in equity, how do one realize or identify stocks around the

circle of competence says for example If someone is into the business of chemicals so how do someone identify the circle of competence with less background in investing?

Ans: So if you are in the chemical industry you have an inherent advantage you understand the supply chain dynamics you can talk to your suppliers you talk to your business partners so you know the end-to-end chain and the trade channel and so on.

That is giving you some edge but investing is slightly different so you have the domain knowledge but then what is suggested is such a person should start attending AGM and start attending con calls.

Start reading the controls of not only the companies that you want to invest into but as many as possible within that sector and try and connect your thoughts in terms of where the puck will likely be not where it is today you don't make money from historic earnings market rewards the future potential or the Delta relative to the valuation.

So you need to understand where the puck will likely be and for that, you need to, unfortunately, do some hard work and go through the Con calls go through the annual reports, AGM and if you're not confident there is no shame in investing through mutual funds, to begin with, and have your own logbook of your learning and then take notes through these channels.

Management

So having skin in the game: is important so management should have some material ownership of the business and typically Sajal Kapoor says he go for nothing less than 30% in the Indian context but he may prefer less globally, so if it's a well-diversified large business like a Lanza or the GSK or a Unilever he doesn't care because they're professionally managed managers.

He won't care about the promoter stay because the promoter is usually a sleeping entity in those businesses but talking more from an Indian context he thinks 30% is the sort of the threshold minimum threshold that he has used and usually comfortable.

Walking the talk by this he means management could talk the talk in an endless manner but if they are not actually implementing and not following it up with some concrete action or ground then that that doesn't make sense.

How to validate? Sajal Kapoor suggests going through the con calls or past annual reports and where they show an example further down and you need to go back five-ten years look up the annual reports and if the con calls, just randomly pick up and try and connect the dots that you know what the management was telling say in 2010 or 2015 and how much of that has actually transformed into implementation and action in terms of taking the business forward.

So that's another critical point and also how do they react to stock movements if the stock price is correcting how do they react if the stock price is rising how do they behave and some see that on the annual report they say their market capitalization has gone up by some percent or in the next five years they want to be at a certain market cap as the management.

So be wary of them, management cannot control that. It's not within their sort of powers they cannot control the external environment they don't control the cycle, they can just control their balance sheet.

So if management is quoting some sort of growth it's an important sort of red indicator if the management is talking about a more interested in a stock price and also listen to their interviews and see how they interact with the stakeholders how they answer queries on the con calls and what's been there a capital allocation track record you get it from the ROCE and that type of thing any known integrity issues of fraud just do google talk to people and you will get some sense there and lastly what about their strategy, is the strategy been consistent or not?

Let's take the example of Biocon, Kiran Majumdar she is active on all social platforms and people find it inappropriate but her goal is to develop blockbuster molecule, ones that could benefit the masses so it's all about affordable innovation and look at the scale of that the business has done right from 50 crores to 318 million in revenues to it's 55 billion rupees and plus in 20 years so a huge scale-up has happened and the chatter and the noise were very negative all throughout but that's where you need to sort of differentiate between the noise versus the voice.

Industry structure

The next sort of pillar the third pillar which is the industry structure and the devil is always in

in the detail so if you read a good book from Pat Dorsey there is also a little book that builds wealth and I remember there was a quote along the lines that moats are always absolute and not relative.

On this company in an instruction effective industry could well be better having a wider mode relative to the best company in a brutally competitive industry like a commodity so that quote from a little book that builds wealth it's a great book I would encourage but superficially when you look at the industry structure you may think that it's all about Porter's five forces.

our suppliers, the threat of substitutes, and so on but it's much deeper and wider than that because there are geopolitical pressures, there are regulatory aspects especially in the industries where Sajal Kapoor invest, like in the chemicals and pharma.

Pharma sector directly is an umbrella industry in itself because you can look at the generics and that will be completely different from API's and then you've got biologics, biosimilars, innovators these small big innovators, virtual biotechs and each of these is a sort of a mini-industry in its own.

Because the five forces and the industry dynamics are very different and so there is no such thing as the pharmaceutical industry, that's the myth there are ten different sorts of industries within that umbrella and you got to have a very clear understanding of the dynamics play out because the dynamics are very different across generics and the innovator even the custom synthesis the content development and CDM or crams as we sometimes each of these sorts of components are very different in terms of the industry structure and when the industry structure turns from negative to positive you make money.

Chemical industry structure was in 2012 because China started withdrawing and the whole structure and something similar happened with the cement industry 20- 25 years ago cement industry today is very stable it wasn't like that in the mid-90s. If you want to trade a stock you have to analyze this stock you know the technicals the head and shoulders and whatnot the cup and fill them all your cycle but if you want to invest you have to analyze the industry structure and the underlying business and then so that's a very fundamental third pillar in my framework.

Business Economics

The fourth pillar that is all about these sort of business economics and all as Charlie Munger says that almost all good businesses engage in pain today and gain tomorrow so you need to invest in capabilities and capacities upfront and the cash will come at a later point in time and this cycle is different for every business.

So the example of a pharmaceutical business if you are setting up a cream-filled facility it's a four to five year gestation period assuming that you are targeting the regulated market the unregulated markets maybe two to three years but no less than that so the capital allocation will not be known tomorrow so if you're putting up a greenfield facility and you want to make complex API's or injectables or the highly regulated markets of Japan and yes it's a five-year game approximately and at the end of that when the cash starts and coming out you would figure out whether the management was right in calling that out.

Understanding the economics of the industry they saw what was happening in the world and implementing it up front in their own companies. Example to go for the backward integration and this is all the size of the opportunity and the other important dynamics in this business economist is the entry barriers because of the opportunity is huge but there are no entry barriers as so for solar industry for the economics of the business will get killed no one would make money you need to worry about the entry barriers and of course, the capital efficiency which is and of course how clean is the balance sheet, because the quality of the business is easy to quantify you look at the balance sheet in a down-cycle at the bottom of this we look at the cash flows.

Psychology

The psychology of the market as well as your own psychology, what kind of investor you are, what are your goals, what are your aims, what are your objectives and you need to align the two so the first thing is to try and understand yourself.

Then decodes that investing lies at the intersection of economics and psychology and the place where the net present value means freedom and greed and fear and everyone is doing this DCF analysis and all the rest of it but these are all about under evaluation overvaluation and the psychology of the market participants from immense fear to extreme euphoria they will keep repeating and if you understand the psychology.

If you understand the business if you understand the domain in which you are playing inside a circle of competence you can have a reasonable estimate not an accurate estimate reasonable, an estimate of the likely value of that and if the market is giving you a good opportunity to buy and you move because if you see that this is a significant discount because of the market and excelling or whatever and if there is an extreme euphoria.

Narrative and Numbers

The narrative must be seen in numbers ( over the period )

CFO has to compound overtime

Market value= NPV of future cash streams

Narrative and Numbers and this is something that has evolved in recent years and that the narrative has to match the numbers The numbers have to match the narrative one without the other is not game. Mostly in pharmaceutical business ratios like CFO/EBITDA, not less than 0.6 or we can track enterprise value or operating cash flows, ROE or ROCE, WACC, CFO or FCF, EV TO CASH SALES.

Don't invest or liquidate.

Look at the enterprise value you look at the operating profits you look at the cash flows and you look at for a better ratio so typically in anything less than 0.6 for CFO to EBITDA is a red flag.

Some companies so jubilant Life Sciences for example did this propose at 250 or something recently but if you look at the CFO to a better ratio for jubilant Life Sciences is one of the best in the industry it's 0.8 you almost have to match the narrative and try to just extent.

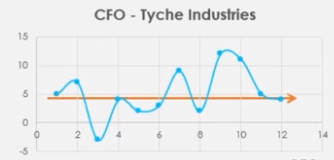

The other example is the Tyche Industry. They haven't done anything else far as the cash flow is concerned the stock may be busing along. It was buzzing around yesterday as well and it's an industry company. But the highlight that looks if you look at their operating cash it has done nothing from point to point it has done nothing it has it's up and down but it should be a gradient of 30-40 degrees right something like this.

One Another is positive Solara pharma again early listing only two-three years of cash but they started scaling up quite well and that's what is likely to see in the businesses that over time the cash should be growing because see if you are getting good operating cash flow and if the management is prudent they can find some growth Capex and opportunities to utilize that cash it could be an M&A it could be an organic initiative. so focus has to be on the balance sheet focus has to be on the operating cash flows.

Cycle and Valuations

Refrain from valuing business on P/E or P/B when the past few years have been miserable or wonderful.

Instead one should focus on EV/Free Cash Flow or EV/OCF.

The final pillar is all about this cycle and evaluations and so there are multiple cycles that come into play. There's always that GDP or the economic cycle is a concrete cycle and the most important cycle is the business cycle because The business cycle is about to turn, where the market cycle is or the economic cycle is so the economy may suffer but pharmaceutical chemical companies may do relatively better even as opposed to some of the more and heavy industrial sectors that are heavier and they need the real economy.

You know the CAPEX play for example and so the business cycle you need to understand the business cycle that where is it in the business cycle if the capacity has been extended or expanded for some niche launches and the business is about to turn into a positive cycle and regardless of where the market of the economic cycle is the gains will flow if the market cycle is conducive and is helping that are a couple of extra percentage point view gains but 80% of the gains will come from the business cycle you get the business cycle wrong and you cannot make money regardless of where the economic cycle is regardless. The business cycle is very important and again you get it from Con Calls, annual reports, and the AGM.

The business cycle used to be a 6-7-year-old cycle you don't know actually the business cycle will last for three years or one years or five years. How do you deal with that predictive model and whether you can actually predict the business cycle anymore?

So you cannot time the cycles if they are getting shorter and shorter so that's a very valid great point in fact the way the cycles are getting shorter but you still cannot predict it is a good thing in the sense that generation takes a lot of based out of companies start and getting more frugal people are realizing that a lot of the cost can be taken off the P&L because things can be done remotely and so on so the new world will look very different.

The cycles are getting shorter and they are very credible and because they are unpredictable you should try and predict what you can do which is again balance sheet and cash flow and sheet in cash flow but that's ROA, ROC metrics.

So the business that has the potential to keep the weighted average cost of capital down has the potential to incrementally improve the ROA & ROC through fresh and CAPEX or internal improvements and has the capability to compound the cash flow.

That will create wealth. It will create a lot of wealth if you are prepared to hold such a business for a longer and duration and don't worry about the day to day price generation because in 10-20-30% of all coming understand the business have a conviction to understand the industry structure and follow some sort of framework.

If you are too much obsessed with the numbers and the ratios you will unlikely make a serious success. As Peter Lynch was one of the early guys that Sajal Kapoor started following, read his books and he has got immense respect and credibility.

But Sajal Kapoor has a framework more on the investing side and to build that knowledge you would have to start from somewhere so again he says keep reading, keep reading, about the business keep reading about other businesses in the same sector, and pick just one sector.

Keep repeating the same thing for every sector you pick and follow the same rigorous process every time.

Thanks to Face2Face hosted by Vivek Bajaj Co-Founder of stock edge & Elearnmarkets.com.

It was a great and insightful session from Sajal Kapoor, a must-watch session.

Looking forward to learning from you, sir.

Twitter Handle: @shuchi_nahar

Very aell consolidated...

ReplyDeleteMadam, sajal sir had given another presentation/ session on CDMO/CRAMs... Do write a blog on it also.. Thanks

Well*

DeleteThank you madam. It was a perfect revision of Sajal Site's ideas & concepts. Thank you for the CDMO article too. Pls keep writing on these lines mam

ReplyDelete