Natco Pharma - Pioneer of Indian Oncology Market - Company Overview

1. Company

Profile

Natco Pharma

(NPL) is a vertically integrated pharmaceutical company having presence in

multiple speciality therapeutic segments. Over the years, the Company has

developed an innate ability to deliver molecules, which are complex and hard to

manufacture. The Company has constantly innovated and manufactured speciality

medicines and niche pharmaceutical products.

The company

also has a US retail business. It owns 8 manufacturing facilities including 6 formulations

facilities and 2 API facilities. Overall revenues grew at a CAGR of 15.4% in

FY16-20. Natco is a leading domestic player in the oncology space. NPL’s

product pipeline consists of drugs, which are used for various types of cancer

like blood cancer, breast cancer, brain cancer, ovarian cancer, lung cancer and

prostate cancer. Currently, Natco is marketing 33 oncology products in the

Indian market (FY20).

2. Management

Guidance

The

management has charted a new growth roadmap with recent entrance in the agrochemical business. Subsequently the

company filed a broad-spectrum insecticide, Chlorantraniliprole (CTPR) in India

for which it expects approval from agricultural ministry shortly.

The company

has invested ~100 crore in this segment till date. Additionally, the company

has filed another Agro product (undisclosed) recently. Overall, the management

expects this segment to contribute ~10-15% of overall revenues 2-3 years

down the line. The Investment is done for following purposes.

· Veda - to get insight of agrochemical

distribution.

· OMRV - for getting an understanding

of the hospital space.

· AACT - for oncology drug discovery.

3. Key

Products in the Portfolio

Para-IV Filing Products in The Pipeline about

to get Approvals and Launch in next few Years.

Focused

approach in US Natco has carved out its own identity via tie-ups to tap limited

but niche products pipeline including 20 Para IVs filings (FY20). As per the

revised and more feasible game plan, it plans to market products via tie-ups

with established players in the generic space.

Till FY19,

the company had filed 51 ANDAs, which includes some niche FTF opportunities.

Overall, the management expects one or two complex product launches in the US.

4. New Launches

in CND/Oncology to Drive Domestic Revenues

Natco is a

leading player in the domestic oncology segment with a product basket of

33 products (FY20). Company expect momentum in oncology segment to

continue on the back of incremental launches amid pricing pressure in some

products. New launches in cardio/diabetology segment (CND) is also expected to

support overall growth. Going ahead, the company is looking to launch six to

eight products a year.

The

company has launched around 5 products in Q1FY21 and plans to launch

cumulatively 10-12 products in FY21 domestically. R&D productivity is lower amid

Covid-related challenges. The company has adequate capacity for Oseltamivir

across two sites (one in India, another in US). Good pipeline of oncology

products. Focusing on chemistry-based molecules as opposed to monoclonals (mAb).

5. Products

That Will Drive Future Growth

Driven by 3-4

products such as Copaxone, Doxil, Lanthanum carbonate. Export growth due to

stocking of two main Covid products. Oseltamivir + chloroquine (Lower margin

products). API growth also led by demand for these APIs. Agrochem – 10-15% of

revenues over next two to three years.

Niche high

value – 3 registered (1 being CTPR), some in pipeline (a) CTPR can be launched

in the Rabbi season depending on court rulings and approvals. Commodity

products – more than 6 filed. Over the next 2-3 years domestic agro business to

grow significantly, maybe start exports. Over 30% market share in Copaxone. Non-US

subsidiaries contributing ~12-13% to consolidated earnings.

6. Revenue Growth

Trend over the Years

7. What Makes Natco Face in the Crowd?

Differentiated

model - Natco

followed a different path for the US market – targeting select opportunities

with limited competition translating into high margins and generating

significant cash flows.

The product

portfolio is focused on complex products or litigation related opportunities.

Natco’s successfully delivered four key opportunities Tamiflu, Doxil, Fosrenol, Copaxone which the company commercalized through its partners over

a 11-month period from Dec-2016 to Oct- 2017.

8. US Filings

Summary in Brief

Company has mapped

16 product filings. These products fall into three categories:

(a)

Opportunities with case settlements and reasonably clear launch timelines - Revlimid March-2022, Kyprolis 2027, Nexavar (likely launch post Jan-2020).

(b) Filings,

which in their assessment are not lucrative anymore: Zytiga, Sovaldi, Tarceva.

(c) Filings

which are diffecult to assess, where outcome is dependent on the court verdict

- Pomalyst, Tracleer. In terms of timelines, Afinitor and Nexavar should be

watched.

Revlimid

- The next big US

approval will be Revlimid while there are handful of other US approvals and

launches lined up. In Canada, the trial for Revlimid commenced in July.

Regarding the US filing, the company has responded to all the queries raised by

USFDA and incremental inspection is not expected. The management is hoping for

a positive news by next quarter.

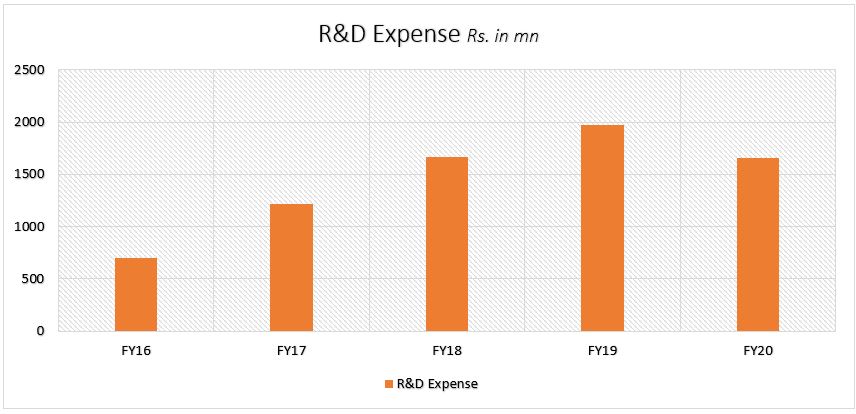

9. Research

and Development – Place where Innovation Happens

Company has

over 40 R&D laboratories in 2 research and development facilities with a

talent pool of over 500 scientists. Company is having capabilities span

synthetic chemistry of small molecules, peptide chemistry, oligonucleotides,

nanopharmaceuticals and new drug discovery. R&D productivity was lower in FY20 amid Covid-related

challenges.

10. Segmental

Overview for the FY 20

Domestic

business: The

domestic business was severely impacted as the Oncology and Hep-C businesses

were affected due to lower demand from patients. The management has

guided for 8-10 product launches in FY21 given the current

situation. On a longer-term horizon, the guidance is 10-12

launches per year.

Oncology

business - NATCO’s product portfolio is among the

most extensive in the Indian oncology market, with 33 active products as on

31st March, 2020. The business was down as immunosuppressed cancer

patients can be highly vulnerable to Covid-19, leading to fewer hospital

visits. The oral oncology business (contributing 65-70% to Oncology business)

is coming back but chemotherapy business (contributing 30-35% to Oncology

business) is yet to be back as the hospital visits are still sparse.

Pricing

pressure is seen easing in this year which was there in 2019. EBITDA margin of

the Oncology business is higher than consolidated company EBITDA margin. The

Company’s revenues from this business segment fell from 3,968 million in FY

2018-19 to 3,078 million in FY 2019-20, primarily due to certain macro

pressures.

Export

business - The

exports (including FDFs and APIs) to the US clocked revenue of 7,834 million

in FY 2019-20. NATCO is positioned strongly in its business in the US, which is

primarily driven by the continued growth of revenue coming from Glatiramer

Acetate and Liposomal Doxorubicin.

The export

business is growing and is offsetting the underperformance of the domestic

business. The business has grown due to company having Chloroquine and

Oseltamivir in portfolio, growth in oral oncology and stocking up due to Covid-19

pandemic.

API - For over two decades, Company has

demonstrated technical and operational expertise in developing and

commercialising more than 40 niche APIs. Company’s key therapeutic domain is

oncology and company is extending expertise

to include CNS and pain management. 49 Cumulative DMFs filed 39 Active

DMFs.

Revenues

from the API division during FY 2019-20 stood at 3,552 million as compared to 3,019 million in FY 2018-19. As of 31st March, 2020, NATCO has a total

of 49 active DMFs with the USFDA for products in the areas of oncology,

cardiology and orthopaedic therapies. Company filed for four DMFs for the US

market in FY 2019-20.

Agrochemicals

business: NATCO has forayed into the agrichemical space through its

Crop Health Sciences Division recently. Currently it is in the process to

complete the manufacturing facilities for both technical (active ingredient)

and formulations.

The company

has filed 1 product and approval takes roughly 10-12 months. The company will

be adopting a similar business model to what it does in the pharma division and

challenging patents will also be a part of business strategy.

China - The company has 4-5 filings under

review in China and couple of approvals are expected in the current fiscal

year.

11. Capital

Expenditure – To Cater the near-Term Demand

During the

year, Company incurred capital expenditure of 3,492.85 million, a majority of

which was used to enhance capabilities in Company’s manufacturing facilities. A

significant portion of this capex was done at their Vizag facility. The

remaining part was primarily used in formulation facilities across the country.

12. Key

Developments

Disclaimer: The information provided on Shuchi Nahar’s Weekend Blog is for educational purposes only. The articles may contain external links , references and compilation of various publicly available articles. Hence all the authors are given due credit for the same. All copyrights and trademarks of images belong to their respective owners and are used for Fair Educational Purpose only.

Reference: Natco Pharma Annual Report & Investor Presentation

Nirmal Bang Research Report

ICICI Direct Research Report

Edelweiss Research Report

Hey Shuchi, was wondering if you took a look at their poor operating cash flow conversion, as far back as 2016.

ReplyDeleteRemove extraneous adjustments and just focus on the operating cash flow; they don't really line up.

Would be interested in knowing about your thoughts.

I found this blog informative or very useful for me. I suggest everyone, once you should go through this.

ReplyDeleteएंटीबॉडी कॉकटेल

Thanks for the posting such a helpful and informative blog post with us. PCD Pharma Franchise is the best franchise business opportunity to the pharma professionals who want to start own venture in the pharmaceuticals industry.

ReplyDelete

ReplyDeleteNice Blog Post, Start your own PCD pharma franchise business at lowest investment.

Great blog post !! PharmaFAQ is the one stop solution for your query regarding pharma franchise, PCD Pharma franchise and Third Party manufacturing service.

ReplyDeleteI read your blog, the provided information is very useful for computer aided drug designing. Keep continue to posting further.

ReplyDeleteThis is a very nice very informative blog post, thanks a lot for sharing, keep it up this good work.

ReplyDeleteOphthalmic PCD Franchise Company

Psychiatric range Pharma Franchise company

Excellent website, Explore pharma manufacturer in India for generic medicines. Innovative is a trusted nutraceutical and pharmaceutical supplier in India.

ReplyDeleteOutstanding website! Explore the top Pharma manufacturer in India for capsules/tablets/syrups. Selecting the right pharmaceutical manufacturer in India is crucial, as a dependable partner guarantees the quality, effectiveness, and safety of the products.

ReplyDeleteStellar website! Seeking for pharma manufacturer in India for oncology drugs. Ikon Remedies is a leading pharma and company renowned for its commitment to quality, innovation, and excellence.

ReplyDeleteStellar website! Seeking for nutraceutical manufacturers in India. Ikon Remedies is a leading nutraceutical company renowned for its commitment to quality, innovation, and excellence.

ReplyDeleteTop-notch website! Seeking for pharma manufacturer in India wholesale. Innovative Pharma is committed to offering premium pharma products that blend traditional wisdom with modern innovation.

ReplyDeleteTop-notch website! Seeking for pharma manufacturer in India for oncology drugs. Innovative Pharma is committed to offering premium pharma products that blend traditional wisdom with modern innovation.

ReplyDeleteTop-notch website! Seeking for nutraceutical manufacturer in India. Innovative Pharma is committed to offering premium nutraceutical products that blend traditional wisdom with modern innovation.

ReplyDeleteOutstanding website! Looking for the nutraceutical manufacturer for health supplements . Ikon Remedies stands among India's leading pharmaceutical companies.

ReplyDeleteFirst-class website! Looking for the pharma manufacturer in India for oncology drugs. Innovative Pharma is committed to delivering high-quality pharmaceutical products that blend traditional wisdom with modern innovation.

ReplyDeleteFirst-class website! Looking for the nutraceutical manufacturer wholesale. Innovative Pharma is committed to delivering high-quality pharmaceutical products that blend traditional wisdom with modern innovation.

ReplyDeleteOutstanding website! Explore the top nutraceutical manufacturer with custom formulations. Ikon Remedies is a leading nutraceutical products manufacturer in India.

ReplyDeleteTop-notch website! Searching for the trusted pharma manufacturer in India for tablets. . Innovative Pharma provides premium pharmaceutical products that seamlessly combine traditional knowledge with cutting-edge Innovation.

ReplyDeleteFantastic Blog ! Discover Nutraceutical manufacturer with organic products . Innovative Pharma is a trusted provider of high-quality pharmaceutical products, nutraceutical products and ayurvedic medicine manufacturer.

ReplyDeleteExcellent Blog. Explore nutraceutical manufacturer in India. Ikon Remedies Pvt. Ltd., established in 2002 and headquartered in Nagpur, Maharashtra, is a leading Indian pharmaceutical company.

ReplyDeleteGreat Blog. Explore the best nutraceutical manufacturer with custom formulations. Ikon Remedies is a trusted manufacturer and supplier of pharma manufacturer and Ayurvedic medicines, delivering high-quality healthcare solutions rooted in traditional wisdom and modern innovation.

ReplyDeleteGreat Site. Explore pharma manufacturer in india for oncology drugs. Ikon Remedies is a trusted pharma manufacturer in India, offering natural and effective health solutions rooted in traditional wisdom.

ReplyDeleteGreat Site. Explore nutraceutical manufacturer in india . Ikon Remedies is a trusted pharma manufacturer in India, offering natural and effective health solutions rooted in traditional wisdom.

ReplyDeleteOutstanding website! Explore nutraceutical manufacturer in Nagpur . Ikon Remedies is a trusted pharma, nutraceutical, and ayurvedic company dedicated to delivering high-quality, innovative healthcare solutions

ReplyDeleteGreat Site. Explore nutraceutical manufacturer wholesale . Innovative Pharma is a trusted name in the healthcare industry, committed to delivering high-quality pharmaceutical, nutraceutical, and wellness products. With a strong focus on innovation, sustainability, and customer well-being.

ReplyDeleteGreat Site. Explore nutraceutical manufacturer in Nagpur . Innovative Pharma is a trusted name in the healthcare industry, committed to delivering high-quality pharmaceutical, nutraceutical, and wellness products. With a strong focus on innovation, sustainability, and customer well-being.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteGreat article! Choosing a reliable Pharmaceutical Manufacturer in India is essential for ensuring quality, compliance, and efficient production. Thanks for sharing these valuable insights.

ReplyDelete